Articles

Hydrogen Economist looks at the new hydrogen projects added to our database and the progress made on existing developments (1)

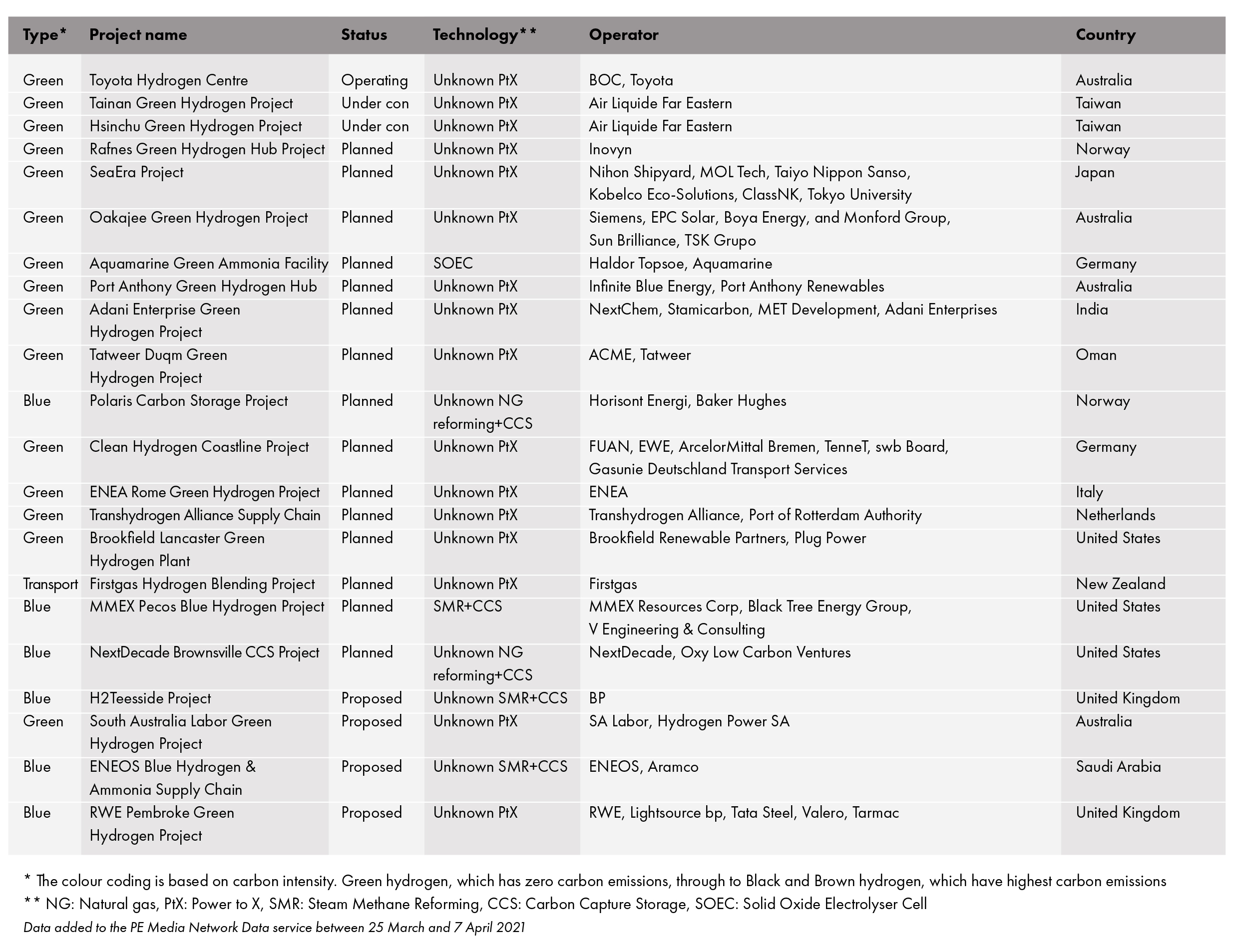

Of the new projects, nine are in Asia-Pacific (Australia, India, Japan, New Zealand & Taiwan), eight are in Europe (Germany, Italy, Netherlands, Norway & the UK), three in North America (US) and two in the Middle East (Oman & Saudi Arabia).

In the UK, BP announced that it is developing plans for the country’s largest blue hydrogen production facility, targeting 1GW of hydrogen production by 2030. The proposed development, H2Teesside, would capture and store up to 2mn t/yr of CO₂ and support the development of the region as the UK’s first hydrogen transport hub. The project is expected to take FID in early 2024 and could begin production in 2027 or earlier, with an initial phase of 500MW. A feasibility study is underway to explore technologies that could capture 98% of carbon emissions from the hydrogen production process. The project could support the conversion of surrounding industries to use hydrogen instead of natural gas, thus decarbonising a cluster of industries in Teesside.

In Taiwan, Air Liquide has completed the first phase of construction on its 25MW hydrogen electrolyser plants in the Tainan and Hsinchu science parks. The plants will be able to produce up to 5,000m³ of ultra-high purity hydrogen per hour. Construction of phases two to five will continue over the next two years. Once complete and supplied with renewable energy, the plants will prevent more than 35,000t/yr of direct CO₂ emissions.

In Oman, Indian solar power producer Acme has signed a deal with Tatweer to set up a large-scale facility to produce green hydrogen and ammonia at Duqm on the Arabian Sea coast. The $2.5bn investment will see the plant strategically planned to cater to international markets for the supply of green ammonia across Europe, North America and Asia, as well as helping to achieve Oman’s Vision 2040 in alternative energy.

Comprehensive details can be found on the Hydrogen Data Service.

Related Articles

Connect with H2Tech