Articles

Hydrogen pathways depend on local circumstances

It is widely acknowledged that hydrogen has the ability to contribute to the decarbonisation of the energy and industrial markets and therefore assist with global efforts to meet emissions control requirements. But for the foreseeable future there will be continued debate about the relative contribution of the various ways to produce hydrogen, differentiated by an associated colour from a palette relating to the environmental credentials of feedstocks and production methods.

For the short- to mid-term, the consensus appears to favour investment in blue hydrogen, derived from natural gas with CO₂ abatement. However, this moves in the longer term to an ever-increasing contribution of green hydrogen, which utilises renewable sources of energy to power water electrolysis.

With hydrogen infrastructure in place… green hydrogen can develop commercially to ultimately supplant blue hydrogen production

The blue variety will facilitate the transition of liquid fuels for hard-to-abate sectors away from high-carbon-intensity fossil fuels to lower-carbon-intensity hydrogen. With hydrogen infrastructure in place, supported primarily by blue hydrogen, green hydrogen can develop commercially to ultimately supplant production of the blue variant, thereby moving from abated-low to almost zero carbon emissions.

Carbon comparison

Understanding the CO₂ emissions performance of blue hydrogen production is important for understanding deep decarbonisation over the longer term. Overall global hydrogen production is responsible for c.830mn t/yr of CO₂ emissions, according to the IEA. Unabated, steam methane reforming (SMR), for grey hydrogen, emits c.9t CO₂ per 1t H₂ produced.

Converting this figure to emissions on an energy-content basis equates to c.60g CO₂/MJ. Therefore, while hydrogen is a clean-burning fuel, SMR has a carbon footprint higher than gas, which emits c.50 g CO₂/MJ at end combustion, but lower than coal at 90-100g CO₂/MJ.

Combining SMR with abatement technology to create blue hydrogen is significantly cleaner. Abatement reduces carbon intensity down to anywhere between 6-35g CO₂/MJ—depending on which stream and what level of CO₂ capture is applied.

Globally, the development of a hydrogen market is progressing. However, the market is still nascent with significant potential technologies remaining in the R&D stage. Commercial production of blue or green hydrogen is limited to a small number of plants located near to the end-consumer. The largest dedicated hydrogen production units with carbon capture, utilisation and storage are:

Air Products’ SMR unit in Port Arthur, Texas. This produces hydrogen for use in the Valero refinery while CO₂ is transported to oil fields for enhanced oil recovery (EOR)

Shell’s Quest project in Alberta, Canada, which produces hydrogen for use in the Scotford bitumen upgrader and injects around 1mn t CO₂/yr into long-term geological storage

There are also a small number of other projects where hydrogen is produced with CCUS, but where the hydrogen is a component of a mixed syngas stream.

Global perspective

Although hydrogen markets will develop across the globe, the initial development of commercialised hydrogen will be defined by national and trading bloc policies in the major economies. The approach and strategy of each country and/or trade bloc differs, and is very much aligned with localised availability of energy resources, energy demand and Paris Agreement commitments.

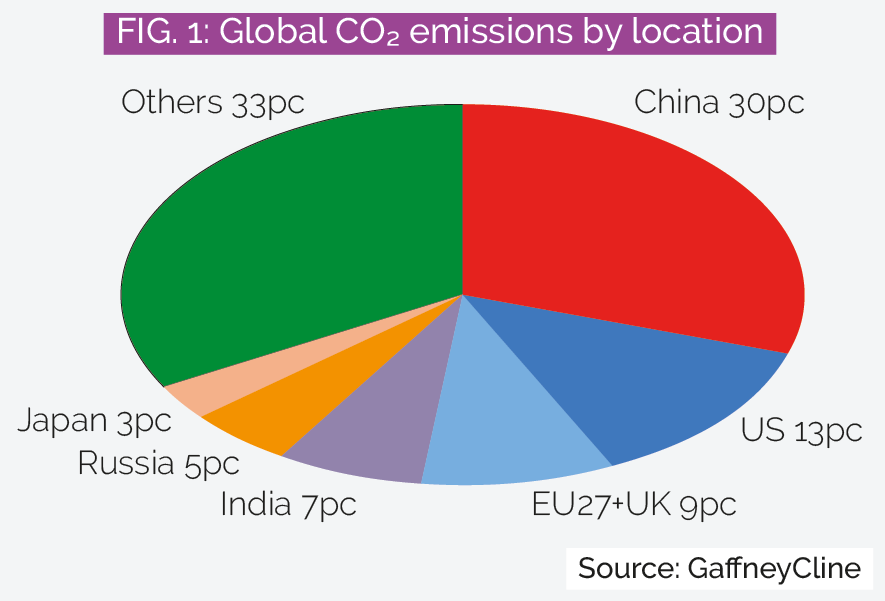

Global hydrogen market development will therefore be heavily dependent on the respective strategies of China, the US and the EU, which in turn reflects a response to carbon mitigation in the main global carbon emitters, namely China and the US, followed in order by the EU, India, Russia and Japan.

Growing competition between the EU, China and US in terms of technological development is also likely to rapidly drive down costs for hydrogen production, as was the case for solar PV development; high-cost solar PV was initially developed in the US and Europe only to move to China for industrial production, resulting in significant reductions in global levellised cost of energy for the technology.

To understand better the global development of a hydrogen market, it is necessary to understand the current focus and drivers in each major economy, as summarised below.

China

China is already a significant player in hydrogen, with an estimated 30-40pc of global production. In terms of regulation, a significant number of hydrogen-related policies progressed during 2020 at national, provincial and municipal levels focused predominantly at the fuel cell vehicle (FCV) market.

Chinese government interest in green hydrogen was considered up to quite recently to be limited, with most hydrogen produced by coal gasification, based on domestic resource availability and commerciality. However, a recent fuel cell and hydrogen infrastructure subsidy policy announced by the central government appears to have provided an incentive to a more rapid green hydrogen market development as part of a focus on the FCV market.

Strategic plans determine strategy in China, with the most recent being the 2015 issue of the ‘Made in China 2025’ plan. This plan focuses on moving China further into high-tech fields, new energy and energy-savings vehicles and progress in new and renewable energy. An associated Energy Saving and New Energy Vehicle Technology roadmap was published in 2016, which focused on FCVs for China’s future energy requirements and business competitiveness, providing targets for specific regions.

The draft of the 14th Five Year Plan (2021-25), to be implemented next year, is widely expected to detail a more extensive development of the hydrogen market, including support for growth in green hydrogen production and technology.

Interestingly, many hydrogen-related policies have been driven by the regional governments, with the central government still to finalise its overall strategy. That said, the central government has recently announced specific FCV-supporting policies. Regional or local governments have also announced a number of hydrogen programmes, typically related to hydrogen infrastructure development. The majority of the stimuli plans relate to FCV and hydrogen refuelling services, although some provinces are looking to develop hydrogen ‘valley’ regional industrial hubs.

The US

The US is at the forefront of hydrogen fuel cell development. It is home to a large percentage of global fuel cell vehicles and a large number of small-scale fuel cell power plants for applications such as remote telecommunications or backup power systems. The US is also home to commercial hydrogen-producing facilities, in addition to having extensive hydrogen-related manufacturing and technological capability.

The federal government provides several tax credits that are applicable for hydrogen-related activities, including investment tax credits under Section 48 (fuel cells) and Section 30B/30C (FCVs and refuelling services).

c.830mn t - Annual carbon emissions associated with hydrogen production

An interesting 2020 House bill committed “the Secretary of Energy to conduct a study to examine opportunities for research and development in integrating blue hydrogen technology in the industrial power sector and how that could enhance the deployment and adoption of carbon capture and storage,” and thereafter to “..submit to the Committee on Energy and Natural Resources of the Senate and the Committee on Science, Space, and Technology of the House of Representatives a report that describes the results...”

The federal government also continues to invest in R&D through the US Department of Energy’s (DOE’s) H2@Scale programme. And the DOE also announced in November the release of a hydrogen programme that provides a strategic view of how it manages hydrogen research, development and demonstration (RD&D) activities. The DOE announced in 2020 c.$64mn funding for hydrogen RD&D projects. Following on from such investment and promotion from the US hydrogen industry, the US government may well implement a more detailed official strategy to mirror those seen elsewhere in the world.

Given the nature of US regulation, each state will also likely progress a range of policies and strategies for future hydrogen market development in parallel with the federal government. To date, there are a number of different enacted energy policies that establish tax exemptions, credits, rebates, loans, grants and corporate income tax credits promoting infrastructure development for hydrogen utilisation.

California, among other west coast states, is at the vanguard of policy development in support of low-carbon activities including hydrogen. Over the last ten years, this has included the Low-Carbon Fuel Standard and the Alternative Renewable Fuels and Vehicle Technology Program, leading into the successor Clean Transportation Program. The California Air Resources Board also provides mandates and funding to zero-emissions vehicles and supporting infrastructure.

The EU

The EU is targeting carbon neutrality by 2050, and hydrogen is a key part of its European Green Deal strategy and action plan, as a potential solution for the many hard-to-decarbonise industrial and heavy transport sectors. The European Green Deal is a package of strategies intended to reduce emissions through implementation of a climate law to formalise strategy, in addition to the revision and review of a number of directives, including strengthening the EU Emissions Trading System, revisions to guidelines on state aid and plans including energy taxation.

The EU Commission last year issued a specific Hydrogen Strategy that prescribes a three-phase plan for hydrogen market development. The EU has the capacity to build a little under 1GW of electrolyser capacity. The first phase of the hydrogen strategy, covering 2020-24, plans for 6GW of electrolyser capacity to produce up to 1mn t of green hydrogen. Planning for hydrogen infrastructure will also commence as well as laying down the regulatory framework for a fungible and functioning hydrogen market, support being provided through appropriate state aid rules.

A second phase, covering 2025-30, calls for 40GW of operational electrolyser capacity, producing some 10mn t of green hydrogen. In this phase, the EU plans to support and stimulate investments for a fully developed hydrogen ecosystem. A third phase is also planned, for 2030-50, but details remain provisional.

The EU acknowledges the role of blue hydrogen in its forward plans as a transition technology for the development of an extensive green hydrogen market. The EU has set out a strategic vision for the share of hydrogen in Europe’s energy mix to grow from less than 2pc to 13-14pc by 2050, the majority as blue hydrogen, promoting growth and employment as well as an intent for global leadership in renewables technology.

In support of the EU plans, funding instruments, such as the Innovation Fund and InvestEU programme, have been developed. These will allow for enhanced investment in hydrogen-related projects. The EU also initiated the European Clean Hydrogen Alliance, comprising both public and private organisations, to facilitate and implement EU strategy.

India

The government of India operates its renewables strategy through the Ministry of New and Renewable Energy (MNRE). A National Hydrogen Energy roadmap was developed in the mid-2000s—but this vision remains distant from what has been achieved by 2020. A major target of the roadmap was for there to be 1mn vehicles using hydrogen on the road by 2020, in addition to a plethora of infrastructure and power generation plans—none of which have come to fruition.

The MNRE is reported to be supporting extensive R&D programmes for hydrogen development, and references two hydrogen refuelling stations, one at an Indian Oil Corporation site in Faridabad and the other at the National Institute of Solar Energy’s Gurugram site.

The government of India in 2015 issued a plan for the development of 175GW of renewable power by 2022. Significant strides are being made in renewable power generation, although hydrogen has not been included in the plans to date. There is, however, much discussion in India with both state and private companies investing in hydrogen technologies, including Indian Oil Corporation, Reliance Industries and Adani. Related ministry officials regularly mention their intent to formalise a hydrogen roadmap, at conferences and to the media, so no doubt policy is being formulated.

Russia

In April 2020, the Russian government adopted a planning document called the Energy Strategy 2035 plan. Russian ambitions focus on the development of the energy sector for domestic economic growth by prioritising the development of internal infrastructure and increasing exports, which are dominated by the hydrocarbon sector.

The 2035 plan cites hydrogen as being important to the Russian energy market, although details are limited. The plan references Russia becoming one of the world leaders in hydrogen production and export. Commentary is included on the diversification of natural gas use; increased hydrogen production from a range of sources; and the implementation of CCUS combined with reforming or methane pyrolysis. There is also commentary relating to increasing the domestic fuel cell market, regulation development and legislation as well as developing export markets. There is also a statement confirming a plan to export 2mn t/yr by 2035.

The Ministry of Energy organised a working group in late 2019 to assess hydrogen development comprising the ministry with representatives of energy-related companies including Gazprom, Sberbank and Rosatom, as well as a number of academic institutions. A subsequent roadmap relating to development of hydrogen energy in Russia for 2021-24 was presented in July 2020 to the Russian government and was approved in mid-October. The roadmap included establishing a regulatory framework for hydrogen comprising state support for R&D, assessment of mixed fuels for power generation and transportation plus hydrogen infrastructure development including new technical and safety regulations, possibly supported by fiscal incentives.

It is clear from the roadmap that Gazprom and Rosatom, with academic support, will be the main conduits for hydrogen development and that nascent Russian hydrogen policies will likely mature rapidly.

Hydrogen is produced in Russia for use in the refining and petrochemical industries, typically on site. Hydrogen technological development has to date been limited and focused on R&D activities, but some new activity has progressed, with Rosatom and Japan's Natural Resources and Energy Agency signing an agreement to develop a pilot project to export hydrogen from Russia to Japan, sourced from electrolysis.

Gazprom and Rosatom are reportedly planning to commence hydrogen production in 2024 with support from the government. There have also been media reports relating to the development of hydrogen-capable turbines and potential hydrogen use in transport infrastructure. A project has been signed between RusHydro and Kawasaki for hydropower-based generation of hydrogen for export to Japan. The potential sale of hydrogen to the European market, either directly or combined with natural gas exports, is also being considered by Gazprom.

Japan

The Japanese government hydrogen strategy is being driven by the Ministry of Economy, Trade and Industry (Meti) as well as the Ministry of the Environment, with significant investment planned in developing a hydrogen-based energy.

Japan imports c.90pc of its energy supplies. Renewables provide only about 10pc of its electricity supply but the country is focused on developing a more robust and environmentally friendly energy mix; Japan is considered as being at the forefront of state support for hydrogen market development.

Japan announced its fourth Strategic Energy Plan in 2014 to initiate its move towards developing a hydrogen-based energy sector. Japan, mostly through Meti, commenced heavy investment in R&D at that time for low-cost hydrogen production, developing a logistics infrastructure in addition to transportation and power generation sectors.

Meti also provides subsidies for fuel cell roll-out as well as FCVs. Japan has also reviewed and revised standards and codes for infrastructure, which has facilitated easier roll-out of hydrogen in certain areas. Local governments are also supporting hydrogen market development, with some subsidies, and the private sector is also involved, with Toyota having commenced commercial production of the first FCV, the Mirai.

The 2014 Energy Plan was followed in 2017 by a hydrogen-specific roadmap, the Basic Hydrogen Strategy. This developed plans and set specific targets to be met by 2030 and proposes a three-phased approach. The main components of the roadmap are:

- Cost reduction, including pricing targets for electrolysers and domestic fuel cell systems

- Increases in FCV numbers over a ten-year period as well as hydrogen fuelling stations

- Development of a supply chain for hydrogen and transport-focused hydrides.

A further roadmap update on hydrogen and fuels cells was issued in 2019, again providing more specific details on targets and plans. A few key items in the roadmap include:

- FCVs increasing in stages from about 3,000, multiplying to 800,000 vehicles in 2030

- 320 hydrogen fuelling stations by 2025

- Over 5mn domestic fuel cells systems by 2030

Japan’s efforts are reflected in a range of hydrogen projects. The Fukushima Hydrogen Energy Research Field (FH2R), completed in March 2020, is a solar PV system producing up to 1,200Nm3/hr. In May 2020, Japan’s Advanced Hydrogen Energy Chain Association commenced pilot transport of hydrogen as an organic chemical hydride from Brunei to Tokyo, supported by both national governments.

More recently, importing liquid hydrogen from Australia has been mooted with the development of the Hydrogen Energy Supply Chain pilot project. This would use hydrogen produced from lignite in Australia, with the intent for carbon capture to be included in the project. The project is scheduled for delivery in a 2022-23 window.

Global roadmap

The global roadmap to a low-carbon future supported by a hydrogen market to help mitigate hard-to-abate sectors is at the very early days of development. Major economies’ policies and focus will be the determining factors of the hydrogen market’s growth rate. These policies are varied and at differing levels of maturity, but the intent to progress hydrogen market development is a strong common element of all major economies’ strategies.

Drew Powell is projects director at GaffneyCline

Author: Drew Powell

Related Articles

Connect with H2Tech